The pandemic work-from-home era may have started the demise of the city office space, but the Biden administration’s spending spree is surely going to finish it off with its resultant inflation and shaky response to a teetering banking system.

Where the trend for decades had been building bigger, glitzier office spaces, sub-leasing the excess to smaller outfits wanting that address near the action, and investors threw money at all of it – the firms building and the firms occupying – now the reverse is true. And there’s a whole lot of shakin’ goin’ on.

Commercial Real Estate Is The "Boa Constrictor" That Will Crush The Economy And Force The Fed To Panic And Restart QE https://t.co/m6VfrQ5Co4

— zerohedge (@zerohedge) April 15, 2023

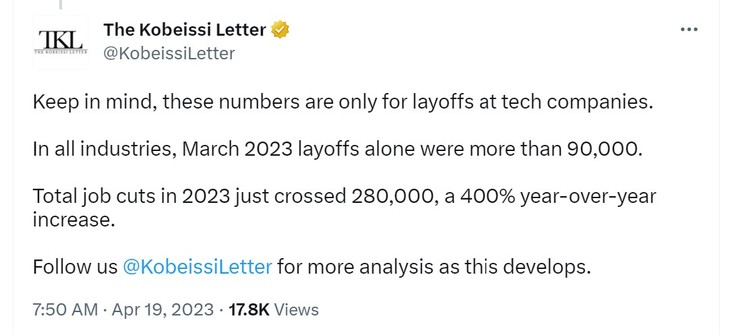

There are a number of moving parts to this ballet. The most obvious is the economic downturn. With just the tech companies alone, like Meta, Amazon, Twitter, etc., laying off tens of thousands of people, the impacts are enormous.

Largest Tech Layoffs Since November 2022:

1. Amazon: 27,000 employees

2. Meta: 21,000 employees

3. Google: 12,000 employees

4. Microsoft: 10,000 employees

5. Salesforce 8,000 employees

6. Dell: 6,700 employees

7. Twitter: 80% of employees

8. Uber: 30% of employees

9. Coinbase:…— The Kobeissi Letter (@KobeissiLetter) April 19, 2023

Some of them had their own campuses and put that space back into the market when employees started working from home. Also much of the collateral damage from those layoffs – the jobs lost because of the effect those layoffs had on the local scene – means that smaller firms are going under. Taking in the bigger picture, it could be said the Biden economy generally sucks.

When it comes to the facilities a business in distress is located in, you can try to move out of the expensive lease or simply throw in the towel and shut the doors.

That’s what’s happening now, especially in the bigger cities, with vacancy rates soaring in commercial real estate (CRE). There’s a boatload of empty square footage.

…That is in large part due to soaring office vacancies in many cities. In downtown areas, the office vacancy rate reached 17.6% in the last three months of 2022, up from 13.8% two years earlier, according to the real-estate services firm CBRE. Despite talk among some policy makers about turning offices into apartments, many investors say that offices would be harder to convert than some other types of properties such as malls.

The majority American corporate offices are currently half-empty, per CNN.

— unusual_whales (@unusual_whales) April 19, 2023

It’s even more dire in places like San Francisco, where their downtown vacancy rate has already reached an astonishing 30%…

The news and the numbers are grim for Downtown San Francisco’s office market—and no one can say with any certainty where the bottom is.

In the first quarter of the year, office vacancies were the highest ever recorded, according to real estate broker CBRE. The firm estimated a 29.5% vacancy rate last quarter, substantially higher than rates seen during the dot-com bust and Great Recession and a seven-fold increase from the start of 2020.

Real estate analysts are expecting vacancies to tick up further as leases—including a major glut of shorter-term subleases—expire in the coming years. More dominos could fall if building owners, faced with lower revenues, decide to hand over their properties back to lenders, many of whom are already-distressed regional banks.

…and everyone knows that’s nowhere near a bottom yet.

…“We’ll have a turnover unlike anything in the history of commercial real estate in the next 12 to 18 months,” said Mark Ritchie, a commercial real estate broker with Ritchie Commercial.

…Subleases, in particular, often offer rent discounts, more flexible lease terms and lower costs to get the office ready for occupancy. But that doesn’t mean sublease offers are flying off the shelves.

Derek Daniels, research director at Colliers real estate company, said that sublease space would typically be on the market for five to six months before being snapped up or pulled off. But throughout the pandemic, that time has dragged out to around 14 months today.

The sub-leasing may have staved off disaster for a little while, but there aren’t enough being leased to begin to cover what’s already available on the market now. And in a year and a half?

Catastrophe if something doesn’t change fast.

…Adding to the problem, many of today’s San Francisco subleases will expire in the next three years. By the end of 2025, an additional 4 million square feet of space will become available, causing real estate analysts to express concern about the trajectory of one of the city’s leading industries.

In the tech sector, a collapse like SVB’s meant that institutions which would lend money to keep firms afloat are either no longer available – as in defunct – or no longer lending. It goes without saying that this isn’t just confined to the tech industry – it’s happening across the board in commercial real estate. Sources of capital are drying up and what capital is available is expensive, thanks to interest rate hikes. If you need money now to sustain your business, whatever it is, it is going to cost you dearly.

Should you be able to access capital, you are also going to get less than you expected, because your asset – that building – is worth less than what you originally financed it for. That’s a fugly realization – you are on the hook for a building that’s worth, what? Maybe 2/3 or less of what you paid for it and now you’re going to have to pay through the nose interest-wise just to hang on to it?

YOICKS

That is also true for investors in CRE, from banks large and small to pension funds and, believe it or not, insurance companies and building owners. The higher interest rates, decreased property values, and the specter of increasing defaults is scaring the liquidity off which used to be a lifeline.

…A small corner of the U.S. bond market, so-called commercial-mortgage-backed securities, or CMBS, have taken a beating for over a year owing to fears that owners of business parks, high-rises and other office properties could default on loans extended at a time of different work habits and lower financing costs.

That stress only deepened recently after Silicon Valley Bank’s collapse, which raised concerns that regional banks might scale back their risk-taking and become more reluctant to make commercial real-estate loans—making it harder for property owners to refinance existing debt.

…High interest rates have also raised the risk of defaults. Owners with floating-rate mortgages are already making larger debt-service payments, cutting into their cash flows. Some owners with fixed-rate mortgages might have a hard time refinancing their loans at higher rates when they come due in the coming years.

As I noted above, even insurance companies are backing away from CRE.

Life insurance companies, until recently a reliable source of capital for commercial property developers, are turning their backs on office building owners as tens of billions of dollars in office loans come due this year.

Many of these insurers have slowed or stopped making office loans, executives and analysts say, interrupting the sector’s decadelong expansion into commercial property lending. Insurance firms have become skittish about rising vacancy rates and falling rents, reflecting the growing popularity of remote work and return-to-office rates that are still around half the levels workplaces enjoyed prepandemic.

…The retreat by insurance lenders is bad news for building owners at a time when other lending sources have all but dried up. Banks, the largest commercial property lenders, have been pulling back since last summer. Their aversion to commercial real estate intensified after the failures in March of Silicon Valley Bank and Signature Bank, industry participants say.

It affects every aspect, from realtors to city tax coffers.

JUST IN: Opendoor, an online company that buys and sells residential real estate, is laying off 22% of employees.

In their company-wide email, Opendoor cited the “housing market decline” as their primary reason for layoffs.

Meanwhile, mortgage demand remains at 30-year lows.

— The Kobeissi Letter (@KobeissiLetter) April 18, 2023

All this attention is focused on CRE right now because of the resources to capital drying up, the vacancy rates skyrocketing, and one huge number that’s rolling around – the bill’s coming due for a huge chunk of this, with no idea how they’re going to repay or refinance it.

Almost $1.5 trillion of US commercial real estate debt comes due for repayment before the end of 2025, per Bloomberg.

— unusual_whales (@unusual_whales) April 18, 2023

That is known as a “debt bomb.”

It alarming enough to have woken up the crew of our sleepy POTATUS.

…Jared Bernstein, a member of the White House Council of Economic Advisers (CEA), told a Senate Banking Committee hearing that occupancy rates in commercial real estate were well below pre-COVID levels and delinquencies had risen a bit recently, although they remained low in historical terms.

“The issue is very much on our watchlist,” Bernstein said during a hearing on his nomination to head CEA, when asked by Democratic Senator Mark Warner about the impact of the collapse of Silicon Valley Bank (SVB) on the sector. The previous CEA chair, Cecilia Rouse, last month returned to her job at Princeton University.

Warner noted that close to $6 trillion in outstanding commercial debt was related to the real estate market, and a “massive dislocation” was under way.

They even added a bit of a concession.

…Still, he conceded that inflation had lasted longer than when the term “transitory” was first used.

“The word is not a helpful term. It’s too ambiguous,” he said.

Nothing about these people is “helpful.”

Feel better yet?

Perhaps it is better the White House is “watching” as opposed to acting.

I mean, their crisis management has been terrific so far.

Join the conversation as a VIP Member