This morning President Biden got out of bed early in order to assure the American people that 1) the banking system was rock solid and 2) that insuring the uninsured (over $250K) depositors of failed Silicon Valley Bank wasn’t going to cost us a single dime.

No, sir, not a dime.

"Can you assure Americans that there won't be a ripple effect? Do you expect other banks to fail?"

BIDEN: *shuts door*pic.twitter.com/OuszLHyFyV

— Tommy Pigott (@TommyPigott) March 13, 2023

I’m not being snide either, about an early morning for our geriatric chief executive.

Psaki: “President Biden does nothing at 9 AM… The fact that he [giving a speech about the bank failure] at 9 AM speaks to how vital the White House recognizes it is.”

pic.twitter.com/mZxMAsUW9j— Greg Price (@greg_price11) March 13, 2023

And then he hot-foots out that door like a man on a mission. Rarely does he move with such purpose.

Everyone was trotting out the line by Sunday afternoon that bailing out making ALL depositors whole was the right thing to do, and somehow, wasn’t going to cost anyone else any money.

Just to be clear none of this money is coming from taxpayers. It’s coming from a tax on banks that funds the FDIF. We should raise the premium payments for banks to protect depositors for payroll & regional banks and to prevent consolidation. That is progressive policy! https://t.co/oeG4wva8Mc

— Ro Khanna (@RoKhanna) March 13, 2023

The answer, as always, is smoke. Once again Biden and company are blowing smoke.

Where does this idiot think taxpayers put their money? https://t.co/PUBDZSSg34

— Frog Capital (@FrogNews) March 13, 2023

As for Rep Ro Khanna’s “tax on banks” funding the FDIF insurance that will pay for all these razzle-dazzle funds without impacting anyone – there’s an interesting SVB twist to that. There could have been a good deal less DIF money available had SVB themselves prevailed last year when they went to war against increasing those very same fees. Don’t you know they were much too burdensome for the bank? Especially for a bank with such low risk, said SVB lobbyists.

That’s the argument in a nutshell.

In the months before Silicon Valley Bank’s collapse, the bank’s lobbying groups fought a proposal requiring financial institutions to increase payments into the Deposit Insurance Fund that protects depositors from bank failures, according to federal records reviewed by The Lever.

As lawmakers now face calls to expand deposit insurance to stave off a wider bank run, the battle shows why that insurance has remained limited — and why any new initiative to require banks to pay for more such insurance could face obstacles in Washington. Put simply: Powerful banking interests and their allies in Congress have made clear they oppose measures that would force banks to pay higher premiums in order to fund depositors’ insurance.

…Lobbying groups representing Silicon Valley Bank, or SVB, argued that risk of bank failures is low and insisted that requiring banks to pay more into the fund would harm financial institutions’ bottom lines.

…At the time, the Deposit Insurance Fund (DIF) had less than $126 billion to insure the nearly $10 trillion of insured deposits in America, meaning the reserve ratio was below the statutory 1.35 percent minimum.

Despite maximum pressure from lawmakers, the FDIC finalized the rule last October.

…The FDIC finalized the rule despite the opposition. The banking industry groups that had opposed the assessment — the Bank Policy Institute, American Bankers Association, Consumer Bankers Association, Independent Community Bankers of America, and Mid-Size Bank Coalition of America — called the final rule a “preemptive strike against a nonexistent threat.”

Now, the FDIC is attempting to sell SVB in order to pay its uninsured depositors. At the end of 2022, more than 90 percent of SVB’s $175 billion in deposits were uninsured by the federal agency.

The Deposit Insurance Fund had a balance of $128 billion at the end of 2022, a tiny fraction of the $9.9 trillion of insured bank deposits in the United States.

The FDIC doesn’t have enough to cover insured deposits in the country, and, suddenly, they’re going to insure every deposit?

Even journalists are asking the Fed/FDIC/Treasury cabal, how exactly will taxpayers not be affected by this again?

I asked Treasury this question on a call with reporters this evening. This was their response pic.twitter.com/LeM9clLzmT

— Jeff Stein (@JStein_WaPo) March 12, 2023

When are Democratically concerned, politically connected entities going to be allowed to fail? As in fall flat on their faces F-A-I-L?

…Even though the systemic risk posed by SVB’s failure is nil (or if not, then every bank is systemically important), the Treasury Department and the Fed responded to these howls and guaranteed all the deposits–even though the FDIC’s formal deposit insurance limit is $250,000. You know, .05 percent of Roku’s deposit.

When evaluating this, one cannot ignore the reality that the Democratic Party is completely beholden to Silicon Valley. This is beyond scandalous.

Occupy Silicon Valley, anyone?

Treasury Secretary Janet Yellen insulted our intelligence by assuring us this is not a bailout. Well, it’s not a taxpayer bailout, strictly speaking, because the Treasury is not providing the backstop. Instead, it is being funded by a “special assessment” on solvent banks. Which are owned and funded by people who also pay taxes. And such an “assessment” is a tax in everything but name–because it is a contribution by private entities compelled by the government.

The policy implications of this are disastrous. The whole problem with such bailouts is moral hazard. What is to stop banks from engaging in such reckless behavior as SVB did if they can obtain seemingly unlimited funding from those who know that they will be bailed out if things go pear-shaped?

…No, the failure of SVB is not the scandal here. The scandal is the political response to it. This reveals yet again how captured the government is. This time not by Wall Street, but by tech companies and oligarchs that are currently the primary source of Democratic political funding.

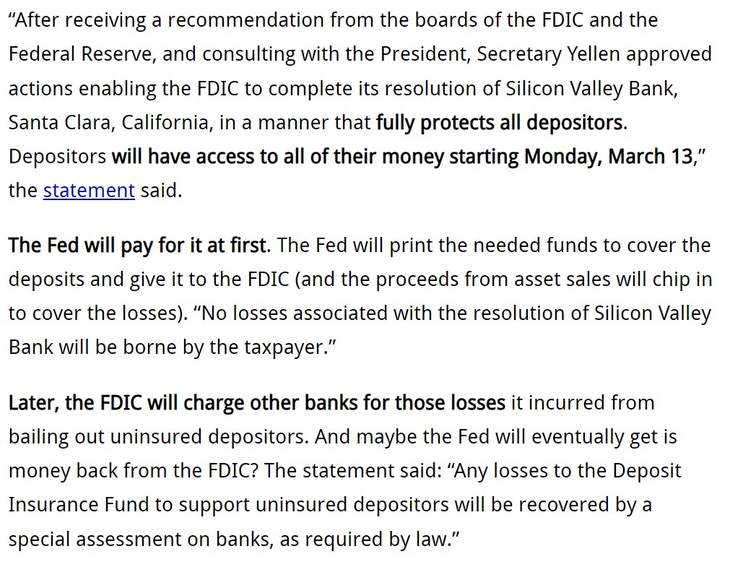

Wolf Street has a nice primer on how it’s not taxpayer money. Well, it is to start. Then sales, fees, recoupments, and hopefully, it gets paid back.

After, RUMOR has it, we get done totally not bailing out Oprah and the Markles, among other ne’er do wells.

Yeah. THAT Oprah and THAT Harry and Meghan.

Feel better?

I sure do. Warm fuzzies.

Join the conversation as a VIP Member