I don’t know why anyone trading in cryptocurrencies would be feeling a little paranoid right now, you know? Especially when the head honchos all seem to have the Alfred E. Neuman “What, Me Worry?” act down pat, with a wink and nudge “trust me, it’s all good” on the side.

Holy smokes.

So in the current climate, a guy in charge of a crypto company, however large or small, should probably be prepared for someone to eventually crawl up his crypto pipe, and ask “who are you?” This is what happened to the fellow who runs Crypto.com, named Kris Marszalek.

CNBC started asking questions and…um…YOICKS.

Kris Marszalek wants everyone to know that his company, Crypto.com, is safe and in good hands. His TV appearances and tweets make that clear.

No one is falling for the “everything’s fine” after Sam Bankman-Fried (aka SBF), the fuzzy-haired slob with the arrested development girlfriend, managed to lose billions of dollars, take other cryptocurrency exchanges/firms down with him and “not have a clue” how it happened.

…Bankman-Fried has denied knowing about any fraud. Regardless, FTX clients are now out billions of dollars with bankruptcy proceedings underway.

Things started going south for Marszalek when the reporters actually took a dig into his previous business experience, something no one had ever bothered to do with SBF, and damn well should have.

…While no evidence has emerged of wrongdoing at Crypto.com, Marszalek’s business history is replete with red flags. Following the collapse of a prior company in 2009, a judge called Marszalek’s testimony unreliable. His business activities before 2016 — the year he founded what would become Crypto.com — involved a multimillion-dollar settlement over claims of defective products, corporate bankruptcy and an e-commerce company that failed shortly after a blowout marketing campaign left sellers unable to access their money.

Court records, public filings and offshore database leaks reveal a businessman who moved from industry to industry, rebooting quickly when a venture would fail. He started in manufacturing, producing data storage products for white label sale, then moved into e-commerce, and finally into crypto.

CNBC reached out to Crypto.com with information on Marszalek’s past and asked for an interview. The company declined to make Marszalek available and sent a statement indicating that there was “never a finding of wrongdoing under Kris’s leadership” at his prior ventures.

The scrutiny was enough considering the circumstances that Marszalek felt he’d best get his side of what was going to be exposed out in the public arena quickly. A Twitter thread ensued.

Helpfully, CNBC translated an acronym in the first tweet I hadn’t run across before – FUD.

…FUD is short for fear, uncertainty and doubt and is a popular phrase among crypto executives.

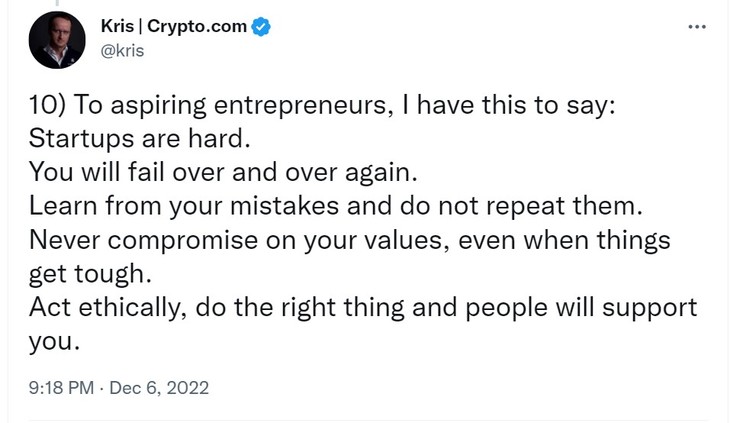

1) More FUD targeting https://t.co/pFc4Pz9nFR is coming, this time about a business failure I had very early in my career. I have nothing to hide, and am proud of my battle scars, so here’s the unfiltered story 🧵

— Kris | Crypto.com (@kris) December 7, 2022

Marszalek goes through 16 tweets combining some details about his various business debacles. Mostly he offers earnest-sounding business advice interspersed with failure and recovery anecdotes. Out of 16 tweets, only 6 have anything to do with his business history. The rest are in this vein.

The comments are mostly positive, “Everybody makes mistakes” kind of cheering the guy on.

As the reporters found, the brief mentions of some – not all – of his less-than-successful wheeling and dealings might leave a few of those in the thread rethinking their ardent support if they had a hint about, as Paul Harvey used to intone, the rest of the story.

For example, the failure of his business out of Hong Kong – it was called “Starline” – is blamed in the thread as being the fault of the financial crisis in 2008, and it eventually drove the firm, and Marszalek, into bankruptcy.

What was uncovered by the CNBC pair is really a wild story. Starline “built hardware products like solid state drives, hard drives, and USB flash drives,” and had to settle with a client’s company for $5M over a shipment of faulty flash drives. The court settlement decreed Starline pay a $1M up front and a $4M credit note to the client.

…Court documents don’t show whether Starline made good on either the $1 million “lump sum settlement fee” or the $4 million credit note. Starline was forced into bankruptcy proceedings by the end of 2009, court records from 2013 show.

Over the course of 2008 and 2009, Marszalek and his partner were transferred nearly $3 million in payments from Starline, according to the documents.

Over $1 million was paid out to Marszalek personally in what the court said were “impugned payments.” His partner took home nearly $1.9 million in similar payments.

“It appears that there was a concerted effort to strip the cash from Starline,” Judge Anthony Chan later wrote in a court filing.

…Marszalek’s representatives told CNBC in a statement that Starline went under because customers failed to pay back credit lines that the company had extended them during the financial crisis of 2007 and 2008. Starline borrowed that money from Standard Chartered Bank of Hong Kong (SCB)….

Yeah. The “financial crisis” did it.

His partner’s uncle apparently helped him settle the Hong Kong bankruptcy and debts. That same partner and uncle helped him establish more businesses in the Cayman Islands.

…Bankruptcy didn’t sever the ties between Marszalek and his partner or keep them out of business for long. At the same time Starline was shutting down, the pair set up an offshore holding company called Middle Kingdom Capital.

Middle Kingdom was established in the Cayman Islands, a notorious hub for tax shelters. The connection between Middle Kingdom and Marszalek and his partner, who each held half of the firm, was exposed in the 2017 Paradise Papers leak. The Paradise Papers, along with the Panama Papers, contained documents about a web of offshore holdings in tax havens. They were published by the International Consortium of Investigative Journalists.

He got involved in a Groupon-type online discount venture that morphed several times, eventually shuttering without paying proceeds to vendors who’d already sold merchandise.

Marszalek’s next move was into crypto, as Foris Ltd.

… Foris’ first foray into crypto was with Monaco, an early exchange.

With a leadership team composed entirely of former Ensogo employees, Monaco told prospective investors they could expect three million customers and $169 million in revenue within five years.

Monaco rebranded as Crypto.com in 2018.

Marszalek was off to the races until this year.

…Crypto.com has laid off hundreds of employees in recent months, according to multiple reports. Questions percolated about the company in November after revelations that the prior month Crypto.com had sent more than 80% of its ether holdings, or about $400 million worth of the cryptocurrency, to Gate.io, another crypto exchange. The company only admitted the mistake after the transaction was exposed thanks to public blockchain data. Crypto.com said the funds were recovered.

Now, with the FTX scandal still causing reverberations across the markets and people’s understandable skepticism about both the lack of oversight and stability of their money (even though crypto was sold to be better and safer than stocks or traditional investment means),

Regulators must step in to protect crypto investors after the collapse of FTX, financial industry executives and lawmakers said at the Reuters NEXT conference this week, the latest call for tougher oversight of a sector prone to meltdowns.

CEOs like Marszalek are being looked at with jaundiced eyes, no longer treated like rock stars with groupies swooning at every utterance no matter how preposterous the individual is on his face. The Wild West for these guys is over. They need to be above board and stand up to the inspection. Mealy-mouthed CYA will only go so far in this day and age, and if you’ve got a trail behind you like this fellow, I’m pretty sure jitters would be a natural reaction from a fair amount of people when they found out.

But they have a right to know and make an informed decision about who they entrust their money to.

A previous record deserves a good look, and crypto cowboys are finding out that due diligence isn’t just another stuffy concept.

A little paranoia can save your bacon.

Join the conversation as a VIP Member